Our fund had a good start to 2024 rising in value by 2.4% compared to the UK stock market which fell by around 1.3%. Over the last twelve months (to end January 2024) our fund (from a total return basis) is up just under 17%. This compares to the overall UK market (including dividends) which was up just under 2%. This, we feel, shows clearly that doing all we can to avoid draw downs, results in superior and positive performance. Through acting sensibly to reduce risk, we think we can produce better returns.

We went into the new year fully hedged 1 protected. From our perspective the year end euphoria about the prospects for interest rate cuts and economic growth at the same time seemed unrealistic. As the month unfolded there was an adjustment to what had been an overly bullish year-end rally and the market fell. A pull back in both the level of the market and in sentiment then allowed us to remove our hedge in the second half of the month. This explains how we were up for the month while the market was down.

At the end of the month, we did re-hedge the portfolio. US earnings season was mostly behind us and, we believe that there is still a lot of risk out there. Sentiment has rebounded to levels of optimism that have not led to especially positive outcomes in the past. We intend to navigate this year with notable caution. The yield curve is still predicting a recession (it has been correct in this in seven out of the last seven times that this has happened). Alternatively, if the economic slowdown does not arrive, we cannot see how there can be notable interest rate cuts set against the background of what is in effect full employment. One way or another it seems to us that market expectations for interest rate cuts and or growth are going to be disappointed.

Regarding the potential for a Western world recession, it is worth addressing why this has not happened yet. It was widely predicted to arrive in 2023 and then failed to do so. From our perspective the reason for this is the currently large government spending and deficit levels that are now common across the Western World. In the US the current year projected budget deficit is around 6% of GDP. Governments have kept spending money as if covid is still around. If the US had, for instance, been running a balanced budget (which would be normal and sensible at a cyclical high) then the economy would be some 6% smaller than it currently is. In other words, the recession would have arrived.

This is a political year in both the US and UK, and it is unlikely that anyone is going to try and put their financial houses in order ahead of elections. It is also the case that tax cuts and or increased spending are being promised by the candidates that are in opposition. The government debt and spending levels we are currently seeing could be the economic elephant in the room. They present real risk. Sadly, throughout history it has been very rare for a country to deal with excessive levels of debt ahead of a crisis of some sort. For 2024 this is, to us, the most concerning issue that could come out of left field. If at some point there is a perception of solvency risk in the US or Italy, for instance, this would be very troubling for markets and the economy. If politicians are forced by markets to come to term with their deficits, then this itself would cause a recession.

Quite apart from the Western world economy itself, the Middle East does not seem to be calming down and it is not entirely clear that China is going to turn the corner either. We expect this to be a volatile and somewhat dangerous year. There is a lot out there for people to be concerned about but for now, (as judged by the currently very positive sentiment levels) people are not scared at all. In our view, this is not a great risk reward environment, and we hope to be able to take a more positive stance once investors are at least a little more nervous than they are now.

We would like to thank all the readers of this letter, and our investors for your ongoing support. We will do our best to defend capital when appropriate and deploying it to make money when it makes sense to do so.

- From time to time, the fund uses FTSE 100 equity futures to protect the value of the fund. When the hedge is applied, net equity exposure is reduced, and the capital should be largely protected. ↩︎

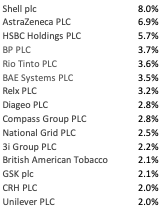

TOP FIFTEEN EQUITY HOLDINGS 31st JANUARY 2024